Dieser Fonds ist nur für den Einsatz in fondsgebundenen Versicherungen erhältlich.

Bitte bestätigen Sie, dass Sie diesen Hinweis gelesen und verstanden haben, um fortzufahren.

Highlights

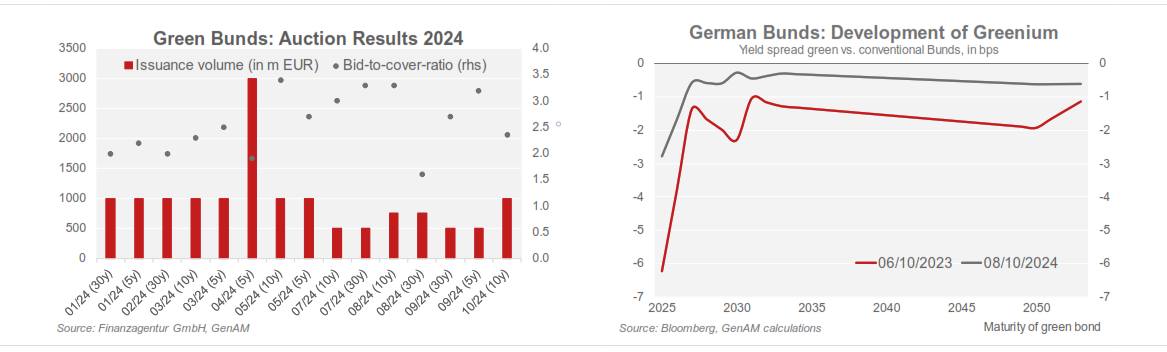

Last issuance of a green Bund in 2024. Germany tapped the green Bund (Germany 2.3$ 02/2033) once again today. The previously outstanding volume of 9 billion was increased by a further billion to 10 billion. As in the previous auctions, the offering met with very solid demand. At 2.4, the bid-to-cover ratio was only slightly below the annual average of 2.6. The average yield was 2.16%. The issuance of green bonds originally announced for November was cancelled, as the volume targeted for the year as a whole has already been achieved with the current issuance. Overall, Germany has thus increased the volume of outstanding green bonds by EUR 17.5bn (slightly more than in 2023: EUR 17.25bn). the average original maturity was just over 14 years. With one exception – EUR 3bn were issued via syndication in June - all bonds were placed at auctions.

Germany strengthens its position as the most active issuer in the euro area. This means that Germany remains the most active issuer of green sovereign bonds in the eurozone. In total, the volume of green bonds outstanding now exceeds EUR 73bn. There are currently eight green bonds, and further expansion to create a complete green yield curve has been announced for the coming years. This means that Germany now also has a slightly higher outstanding volume than France.

Greenium remains positive but tends to fall in a maturing market. Regarding the greenium, the diversity of euro area issuers remains high. The greenium remains generally positive, but the trend is towards a further decline over time. This shows that the market is stabilising and becoming increasingly mature. Most euro area countries have already issued green bonds. This reduces the dependence on a small number of issuers and enables investors to diversify further. The development of the greenium is particularly evident in the case of green Bunds. Due to the twin concept, all green Bunds are always based on a conventional Bund with matching features. In particular, the twin bonds have identical coupons and maturities. However, the green bonds are issued slightly later and have a smaller outstanding volume. Hence, the twin concept makes it easier to determine the greenium and increases the transparency for market participants.

Geenium to persist in future. As the chart below shows, the greenium (except for the bond maturing in 2025) is below 1 bp (at the beginning of 2023, the average greenium was still 5 bp). This reflects not least the steadily increasing supply of green bonds across the entire public sector. However, we do not expect the greenium to disappear completely. Due to the greater transparency of how the proceeds are used, green bonds have a higher value than conventional bonds. In this respect, a greenium can be expected in the future.

This document is based on information and opinions which Generali Asset Management S.p.A. Società di gestione del risparmio has obtained from sources within and outside of the Generali Group. While such information is believed to be reliable for the purposes used herein, no representation or warranty, expressed or implied, is made that such information or opinions are accurate or complete. The information, opinions estimates and forecasts expressed in this document are as of the date of this publication and represent only the judgment of Generali Asset Management S.p.A. Società di gestione del risparmio and may be subject to any change without notification. It shall not be considered as an explicit or implicit recommendation of investment strategy or as investment advice. Before subscribing an offer of investment services, each potential client shall be given every document provided by the regulations in force from time to time, documents to be carefully read by the client before making any investment choice. Generali Asset Management S.p.A. Società di gestione del risparmio may have taken or, and may in the future take, investment decisions for the portfolios it manages which are contrary to the views expressed herein. Generali Asset Management S.p. A. Società di gestione del risparmio relieves itself from any responsibility concerning mis- takes or omissions and shall not be considered responsible in case of possible damages or losses related to the improper use of the information herein provided. It is recommended to look over the regulation, available on our website www.generali-am.com. Generali Asset Management S.p. A. Società di gestione del risparmio is part of the Generali Group which was established in 1831 in Trieste as Assicurazioni Generali Austro Italiche.

© Generali Investments, alle Rechte vorbehalten. Diese Website wird von der Generali Investments Holding S.p.A. als Holdinggesellschaft der wichtigsten Vermögensverwaltungsgesellschaften der Generali Gruppe zur Verfügung gestellt, die direkt oder indirekt die Mehrheitsbeteiligung an den unten aufgeführten Gesellschaften hält (im Folgenden gemeinsam "Generali Investments"). Diese Website kann Informationen über die Tätigkeit der folgenden Gesellschaften enthalten: Generali Asset Management S.p.A. Società di gestione del risparmio, Infranity, Sycomore Asset Management, Aperture Investors LLC (einschließlich Aperture Investors UK Ltd), Plenisfer Investments S.p.A. Società di gestione del risparmio, Lumyna Investments Limited, Sosteneo S. p.A. Società di gestione del risparmio, Generali Real Estate S.p.A. Società di gestione del risparmio, Conning* und unter deren Tochtergesellschaften Global Evolution Asset Management A/S - einschließlich Global Evolution USA, LLC und Global Evolution Fund Management Singapore Pte. Ltd - Octagon Credit Investors, LLC, Pearlmark Real Estate, LLC sowie Generali Investments CEE. *Einschließlich Conning, Inc, Conning Asset Management Limited, Conning Asia Pacific Limited, Conning Investment Products, Inc, Goodwin Capital Advisers, Inc. (zusammen "Conning").